CommentsDEMOCRACY NOW-We speak with investigative reporter Aaron Glantz about his new book “Homewreckers.”

It looks at the devastating legacy of the foreclosure crisis and how much of the so-called recovery is a result of large private equity firms buying up hundreds of thousands of foreclosed homes. “Homewreckers: How a Gang of Wall Street Kingpins, Hedge Fund Magnates, Crooked Banks, and Vulture Capitalists Suckered Millions Out of Their Homes and Demolished the American Dream” reveals how the 2008 housing crash decimated millions of Americans’ family wealth but enriched President Donald Trump’s inner circle, including Trump Cabinet members Steven Mnuchin and Wilbur Ross, Trump’s longtime friend and confidant Tom Barrack, and billionaire Republican donor Stephen Schwarzman.

Glantz writes, “Now, ensconced in power following Trump’s election, these capitalists are creating new financial products that threaten to make the wealth transfers of the [housing] bust permanent.” Aaron Glantz is a senior reporter at Reveal from The Center for Investigative Reporting. He was a finalist for a Pulitzer Prize this year for his reporting on modern-day redlining. (Slightly edited for clarity.)

AMY GOODMAN: We now discuss a new book that looks at the devastating legacy of the foreclosure crisis and how much of the so-called recovery is a result of large private equity firms buying up hundreds of thousands of foreclosed homes. In it, Aaron Glantz reveals how the 2008 housing crash decimated millions of Americans’ family wealth, but enriched President Donald Trump’s inner circle, including Trump Cabinet members Steve Mnuchin and Wilbur Ross, Trump’s longtime friend and confidant Tom Barrack, and billionaire Republican donor Steve Schwarzman.

What an amazing book! Just lay out what you found.

AARON GLANTZ: Eight million Americans lost their homes in the Great Recession. But they didn’t just disappear, right? We live now in a society where the wealth gap between the richest one-tenth of 1% and the other 90% is bigger than it’s been in a hundred years. Much of Americans’ wealth is in their homes because they have very few other ways to save.

I wanted to know: What happened to these houses? Who profited off this mess? That trail led me to a number of people who are in Donald Trump’s inner circle.

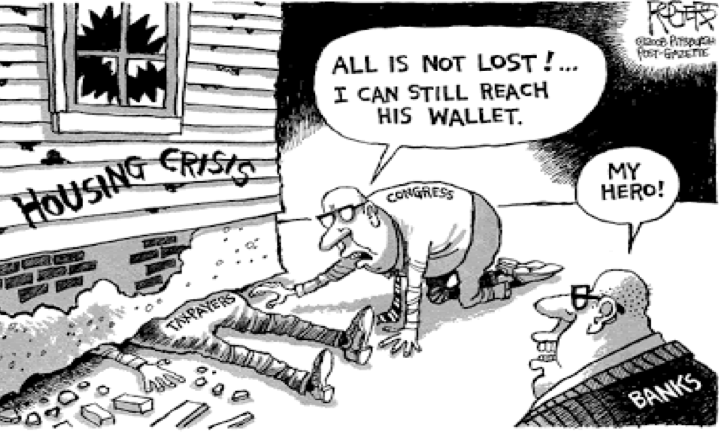

We start with the crash itself and the failure of the banks. When all of these bad loans came due and there were massive foreclosures, we, the taxpayers, through the Federal government, subsidized those foreclosures. There were a lot of people who lost money during that time, but there were also people who bet on these failed banks and received government support to foreclose. That included, as you mentioned, Steve Mnuchin, who’s now our Treasury Secretary. He and his group of other investors, including George Soros, John Paulson, Michael Dell, the founder of Dell Computer, bought IndyMac Bank, a failed Pasadena, California, bank. They then proceeded to foreclose on over 100,000 families, including 23,000 seniors.

Under the deal that he made with the government to acquire this bank, which the government owned because it failed, Mnuchin and his investors paid the government nothing. Then, although he invested some of his own money in the bank, the government paid him to subsidize his foreclosures. And documents that I obtained under the Freedom of Information Act show that the Federal Government paid his group more than a billion dollars. Wilbur Ross, the commerce secretary, had a similar deal at Bank United, which was another failed bank in Florida.

JUAN GONZÁLEZ: IndyMac, as you show in your book, was really the first major bank to collapse, and then a series of others happened in 2008. It was based on a either fraudulent or predatory lending. If you could talk about that, as well?

AARON GLANTZ: There were a lot of predatory loans going around in the housing bubble at this point; we all know that. What I wanted to know was when there were families who got these so-called NINJA loans — no income, no job, no assets, no problem — or these loans that had these teaser rates and then reset at a higher level, and you were told, “Oh, you can just refinance.” The main character in my book is Sandy Jolley. His family owned their home outside of Los Angeles for more than 30 years, until they got a reverse mortgage that sapped their equity — and all of these families lost their homes to foreclosure.

What I wanted to know was what happened after. Right? We’ve been stuck in this country on this trauma of 2007, 2008, and 2009. But now here we are in 2019. Ten years have passed. The unemployment rate is low. The President tells us everything is great. But, people don’t feel like everything is great. We have jobs, but what happened to our wealth? They took it. That’s what happened.

JUAN GONZÁLEZ: The disproportionate impact that this loss of equity in all these homes had, especially on the African American and Latino communities, which were even more dependent on home equity for what little wealth they had or net wealth they had.

AARON GLANTZ: What we see is that banks, like Steve Mnuchin’s bank, concentrated their foreclosures in communities of color. They started making loans again when the economy improved, but they didn’t make loans to those communities. They wiped out the wealth of these communities with foreclosures, but then, over a five-year period, Steve Mnuchin’s bank made three loans to help African Americans buy homes and 11 loans — this is national bank — helped three African Americans and 11 Latinos buy homes over five years.

Now Steve Mnuchin, as the Treasury Secretary, is in charge of regulating every American bank. He and Donald Trump picked one of his deputies at OneWest Bank, Joseph Otting, for the position called Comptroller of the Currency, which basically is America’s top bank cop. He is in charge of enforcing laws, like the Community Reinvestment Act, that are meant to stop redlining. So, this bank, which hardly made any loans to communities of color, is now in charge — under President Trump — of making sure that these anti-redlining laws are followed.

JUAN GONZÁLEZ: It seems to me it’s not just the Trump administration, because it was under the Obama administration there was supposed to be some efforts to help homeowners stay in their homes. In fact, Julián Castro, now a presidential candidate, was at HUD supposedly in charge of the efforts to assist homeowners, and that’s come under heavy criticism.

AARON GLANTZ: Some people say this is an anti-Trump book because it has Donald Trump on the cover holding wads of cash, with Steve Mnuchin riding on a wrecking ball and, Wilbur Ross pulling money out of a house. But all of this activity happened, as you mentioned, when Barack Obama was the president. I started working on it in 2016, when I didn’t know who the new president was going to be. But I noticed that the homeownership rate in this country, instead of going up during the economic recovery, it kept going down. It went down in 2012. It went down in 2013, '14, ’15 and ’16. Until 2016, it bottomed out at its lowest rate in over 50 years. That's when I started asking the question, “Who profited under Obama?”

AMY GOODMAN: Tell us more about Tom Barrack and Steve Schwarzman, their relationship with Trump, and what they did.

AARON GLANTZ: Tom Barrack is Donald Trump’s oldest, closest friend, and he introduced Ivanka at the Republican National Convention. He planned the inauguration for Donald Trump. Steve Schwarzman, another old Trump friend, according to media reports, still has the president on speed dial.

Now, we’ve been talking about the foreclosures. Who bought those foreclosures? We have seen a massive transfer of wealth, as I mentioned, not from one group of families who got foreclosed to another group of families who were able to buy homes. We now have 3 million homes in this country that are owned by LLC, LP and LLP shell companies. Some of the largest buyers of these homes were private equity funds run by Tom Barrack and Steve Schwarzman.

There’s now a company called Invitation Homes, which was founded by Blackstone, Steve Schwarzman’s company. It owns 80,000 homes across more than a dozen states. And it’s a publicly traded company now. They have their IPO. They very clearly track their rent increases and the relatively small amount of money they spend on maintenance. Also, importantly, because these people are leverage buyout kings, they have been taking these homes and bundling them into this new type of mortgage-backed security, taking on a ton of debt. So, for example, I mentioned earlier Sandy Jolley, this longtime homeowner in Los Angeles area whose family owned their home for more than 30 years before they were foreclosed on by Steve Mnuchin’s bank. His home is part of a $960 million mortgage-backed security, bundled with thousands of other homes. If you look at the property record, you don’t see la $20,000 home equity line of credit to remodel the kitchen. You see a $960 million lien on the house taken out by a private equity firm.

JUAN GONZÁLEZ: Aaron, talk to us about John Paulson, another billionaire hedge fund and equity guy, another big supporter and adviser of Donald Trump, and his role in all of this.

AARON GLANTZ: We’ve been talking about Steve Mnuchin, the Treasury Secretary. He bought the IndyMac bank. But he was just the head of a group that bought this bank. Paulson lives in a 6,000-square-foot apartment on Park Avenue, has another house in Bel Air, and another one in Scotland, but that’s not the real money, right? Paulson had made billions of dollars in the run-up to the housing bust. He was one of these hedge fund guys who saw that we were in a bubble, bet against the American dream and made a ton of money. He wondered, “OK, now there’s a crash. How am I going to make money on the way up again?”

His staff studied the S&L bailout. All of these guys looked at the savings and loan crisis of the late '80s, which was another time when the government intervened and bailed out the rich at the expense of the rest of us. They used it as a playbook. One of the things they noticed was that some of the richest deals, the best deals for the hedge fund guys to come out of the S&L crisis, came at the beginning. That's why they bet on IndyMac. But another reason Mnuchin had to put together this group is if any of these hedge funds had put in more than a certain amount of money into the bank in terms of their share of ownership, they would be regulated as bank holding companies. The government would then be able to go in and look at their books. So, they stayed below that threshold to make sure that they would avoid scrutiny.

As I mentioned at the outset, the richest 0.1 of 1% of the American people have the same amount of wealth as the other 90%. That is because in America, 80% of most middle-class families’ wealth goes to only five things: food, housing, shelter, transportation, and healthcare. All those other things, besides housing, just disappear as soon as you spend your money. Housing is the only way that most Americans have to save. The average American family has $4,000 in the bank. So, either you put your money in equity in your house, or you pay it to your landlord. If it’s a private equity firm, it goes on the bond market, or you have a little bit for yourself. I’d like to see the candidates engage on this question.

JUAN GONZÁLEZ: Your book also does talk about some of the regulators who attempted to do the best they could to deal with the bank failures. Sheila Bair, of course, is highlighted in your book. Talk about the regulatory climate right now, in terms of being able to protect homeowners, and the lending industry, in general.

AARON GLANTZ: When I looked at the history of America, the thing that jumped out to me was, in this financial crisis, how many people came, throughout the whole process, with really great ideas that were summarily ignored under President Obama. I write about Alan Blinder, who was a former member of the Federal Reserve Board. In 2008, he went with a number of other prominent economists, including members of the conservative [American] Enterprise Institute, and said, “Hey, you know, what we need is a government-run bank, like President Roosevelt had during the Great Depression,” when the Home Owners’ Loan Corporation helped more than a million Americans keep their homes. It refinanced one out of every five mortgages in urban America. It invented the long-term fixed rate mortgage. And, guess what, it made money for the taxpayers, because the American people paid their loans back. After World War II, we had the GI Bill. It helped 4 million Americans buy homes. It basically broke even, because the GIs paid their loans back.

Instead, what we had over the past decade is this massive government giveaway to private equity and a few people who are now close friends of the president and in his administration. The really scary thing is that under President Trump, these people are running the country. They are, bit by bit, taking away the few scraps and reforms that Obama put in place, defanging the Consumer Financial Protection Bureau, weakening the Dodd-Frank Act, which regulated the banks. We’re seeing, as I mentioned earlier, a ballooning number of this new kind of mortgage-backed security, a $960 million lien on a single house in South Los Angeles. So, this is where we’re at. The people who looted us during the Obama years are now running the country. That’s why the book is called “Homewreckers.”

AMY GOODMAN: We’ve got just 30 seconds. What shocked you most?

AARON GLANTZ: I think the thing that shocked me most was how many of these good ideas were proposed and how much they were ignored over more than 10 years. There really is no reason that we have to be in the situation we are now.

(Democracy Now! produces a daily, global, independent news hour hosted by award-winning journalists Amy Goodman and Juan González. Their reporting includes breaking daily news headlines and in-depth interviews with people on the front lines of the world’s most pressing issues.) Prepped for CityWatch by Linda Abrams.